When you delete things off of a mobile device (like a phone or digital camera), the file goes to your phone’s recycle bin (just like on a desktop computer or laptop), typically an invisible folder named .trashes or .trash. There, it continues to take up the same amount of memory storage as it did before you ‘deleted’ it. To empty your mobile device’s recycling bin, plug your phone into your desktop or laptop via USB as a memory device, right click on your desktop/laptop’s recycling bin/trash, and tell it to empty your recycling bin/empty trash. Your computer will empty all .trash/.trashes folders, including the one on your phone, actually deleting the files permanently this time, freeing up your phone/camera’s memory space. Reblog to save a life.

(I know this works on MAC with my Andriod, it’s not too far a stretch to do the same on Windows and/or with other phones as well. In fact, it should be easier to do on Windows since Windows Explorer is more conducive to finding hidden folders.)

FINDING THIS RANDOM POST ON MY DASHBOARD GAVE ME THE BEST ANSWER TO SHIT I’VE BEEN GOOGLING ABOUT FOR MONTHS!!!

oxford was built and operational as a college before the rise of the mayans and cleopatra lived in a time nearer to pizza hut’s invention than to the pyramids being built

I need a noncomprehensive history book that covers Known World History in time periods, like “in this century, all this shit was happening concurrently” and not just all spread out so I have to piece it together like some unpaid uneducated scholar

Yeah! Like, a chronological history atlas. Each chapter covers 100 years or whatever (probably longer periods the farther back you go), and the start of each chapter is a world map, with brief summaries of all the stuff going on, with page numbers to turn to the relevant section. So you could read Egypt’s sections in each chapter only, and get a decent overview of the history of Egypt, or read each chapter wholly and get a sense of what was going on in the world/on a given continent or whatever.

There would have to be careful organization and good writing to help the reader keep track of people and civilizations that span multiple chapters, so that reading about the Roman Empire in the 100′s BC doesn’t feel totally out of context, and especially for groups of people that moved around a bunch. Probably would be done with footnotes, like, ‘hey, last time we saw these guys, they were over here doing this, see section (page number)’.

Ideally, it would cover political/traditional history (wars, important people, etc.) technological history, and social history. So not only do you know what was going on in China when Augustus was emperor, you also have an idea about how the average Roman or Chinese person lived at that time.

That would be such a huge project and would involve so many scholars but it would be SO COOL

the lesson for today, class, is when to use epithets rather than names or pronouns — and when not to.

USE EPITHETS:

– when the character’s name is unknown, so there’s really no other way to refer to them:

Two goons in suits blocked my way. “You ain’t going nowhere,” said the ugly mook. The even-uglier mook just grinned.

– to draw attention to the role or function described:

Bill was so excited to meet Obama, he was a little worried he’d end up remembering today as the day he threw up on the president.

– as in-character commentary to flesh out the POV’s voice:

You stand back and nudge the door open with your toe in case of falling buckets, but it seems the windy dipshit has given up on that particular tired prank.

(NOTE: use this last one SPARINGLY. consider your own internal monologue. how often do you think of people by anything but their names? too much of this trick breaks immersion.)

DO NOT USE EPITHETS:

– to avoid using pronouns.

– to avoid using names.

– to remind the reader of physical characteristics you should’ve described elsewhere.

– to remind the reader of physical characteristics they already know perfectly well because they wouldn’t even be reading your damn fanfic if they weren’t familiar with canon, come ON people.

– to try to sound erudite or poetic.

– for any other stupid reason. i’m serious. i will come over there and hit you.

– i’m not kidding.

– fucking stop.

Yes. READ THIS PEOPLE.

^^^^^^

It bears repeating, fic writers: if you’re thinking about using an epithet because you fear you’re being repetitive, YOU ARE NOT. Trust me.

Everyone would much rather read “Draco” or “Steve” than “the tall blond” or “his blond lover”.

This forever! This forever and ever! Using epithets in the above fashion is an instant back button for me personally. Please never ever write ‘the blonde’ or ‘the blond man’ I beg of you!

Okay so I really love this one because the OP begins with times when epithets are actually useful, instead of just universally panning them. And the thing is, they can be tremendously effective. Just … probably not the way most folks use them ;-p

So if you lived in a society where you had to secure your communication in order to be yourself around others, here are the apps that could help you do that.

Signal let’s you securely text and make phone calls.

Onion Browser allows you to surf the web without leaving a trail.

Duck Duck Go isn’t super secure but it won’t record your searches like Google.

ProtonMail is a email client that lets you email other secure email accounts.

Periscope allows you to stream live video.

Semaphor is there so you can securely make group chat rooms.

American privacy laws allow you to use these all. So that’s pretty cool.

Because we’re currently living in the prologue of a cyberpunk dystopian novel, imma reblog this.

Okay, at this point there has to be something wrong with me, right? I’ve watched this 20 times in the last half hour, I still don’t know what they are saying half the time, but it doesn’t seem to matter because i’ve been crying my eyes out laughing for the entire last half hour …

what the fuck is this from i gotta know

it’s called letterkenny and it’s about a man who gets dumped and then goes on to shirk his pacifism and reclaim and hold his title as the toughest dude in the rural town of letterkenny ontario. every episode cold opens like this in increasingly bizarre ways.

I read the bit about not being able to parse what’s being said and then I read the bit about it being set in this fuckin province, and I thought, like, what kind of accent could they possibly use that was so incomprehensible while still setting it in northern goddamn

Ontario? and actually, okay, you know what, despite having lived immersed in it my entire life I’m not sure i’ve ever seen this exact accent on tv before, it is just weird to see actors using it

My cousins grew up with the guy who wrote this show and is the main actor. It’s scary accurate for hick town Ontario (it’s based on the town of Listowel) and apparently some of the characters are based so closely on real people that they’ve recognized themselves while watching.

ARE YOU GONNA FIGHT IN THOSE SHADES OR PLAY POKER STARS DOT COM

Distribute some free literature.

I lived near Ontario in rural NY and we picked up this sort of similar affect. It’s so scary how true-to-life this is in that area of the contintent

my favorite fucking thing about this is that without context i have no way of telling if it’s flipped or not, but i’m pretty sure it’s read right-left because reading it left-right is HILARIOUS

ok can we agree that the WORST feeling is when you’re just sitting around consciously procrastinating and you’re just overly aware that each second that passes is more time wasted and you like watch hours pass and you’re STILL procrastinating and you CANT STOP and your panicked brain is trapped inside a body that refuses to be productive and inside you’re screaming but outwardly you’re just eating chips

The best thing I know for this is just to do SOMETHING. It’s like you’re in a trance, so you have to break the trance. Get out of your chair and go into another room, or step outside. You don’t have to stay there long, but if there’s something small you can do in that other room, like wash a dish or fold a shirt, do it. If you hate it, you don’t have to do it forever. Then sit down somewhere and just experience the urge to do the procrastination activity but don’t act on it. See if the urge fades a little. If it doesn’t at all, go back to the distracting activity and set the timer for 10 minutes. At that ten minute mark, get out of your chair and repeat the above.

My shrink calls this STOP. It’s a DBT Distress Tolerance skill: Stop, Take a Step Back, Observe, and Proceed Mindfully. Once you get out of your trance, you can shut your eyes, check in with yourself, and DECIDE what to do next instead of just getting carried a long. Don’t pick something HARD to do, pick something very easy but active and that will give you a sense of accomplishment, no matter how small. If you really need to, you can go back to the distracting activity for little breaks but try to set a timer so you don’t get entranced again.

This is hard and takes practice. Maybe the first time, all you’ll manage is getting into the other room and then coming right back. Keep trying. It’s a muscle you build. I leave little notes around my house to remind me to do this. That helps.

Here’s a thing you might do BEFORE all of that. When I’m SUPER anxious and stuck, I’m out of what my shrink would call my Window of Tolerance, which is when you’re so keyed up (or so keyed down) that you can’t really think or act deliberately. So I have a list I keep on my wall: First I stick my face in ice water for about 30 seconds. This triggers the mammalian diving reflex, which depresses your sympathetic nervous system. Then I take a shower, trying to focus only on the water and not my racing thoughts. Finally I sit and do Four-Square breathing for a few minutes, which actually you can do anytime, anywhere. It has a similar effect as the ice-water thing. (If you have PRN anti-anxiety medication, taking a little of that at the beginning of the process can help you get through the exercises.)

Once you’ve calmed down and de-entranced yourself a little, you can possibly think about working again. Pick something very limited and specific. “I’m just going to write ONE paragraph about [x]” or “I’m going to study this one page.” Or “I’m going to work for 15 minutes.” GIVE IT A LIMIT so you aren’t trapped. Then you get a break to distract yourself. Keep the break short, but don’t skip it. You can finish a whole task by just going from one little sub-task to another, without ever looking at it from a whole-task perspective. Just keep doing one more little bit next and eventually you’ll be done.

so it’s open enrollment time, which means you need to pick a health insurance plan from the exchanges! it can be daunting as shit, for sure, especially if you don’t live in the filthy weeds that are the business side of our garbage health care industry like yours truly does.

so! here’s a quick rundown of some of the vocabulary:

premiums: this is what you pay per month for the glorious honor of having insurance coverage. it does not count towards your deductible or out of pocket maximum. depending on your income, you may be eligible for a subsidy or other financial assistance to make your premiums more affordable.

deductible: this is how much in health care costs you have to pay before your insurance starts really kicking in. for example, my insurance through work had a $1,500 deductible, so the copays and coinsurances and lab costs that i had to pay early in the year, before i had another surgery, were fully my responsibility until i’d paid out $1,500; after that, my insurance started covering a flat 80% of everything, including copays. basically, the deductible is how many actual dollars you have to pay out for medical costs before your insurance takes over.

if you’re someone who goes to the doctor a lot, like me, you’re probably going to want a plan with a lower deductible, which will have a higher premium; however, in the long run, you’ll come out more ahead with a high premium/lower deductible.

on the flip side, if you’re generally healthy and just need an annual checkup, flu shot, ob-gyn annual, etc., then you probably want a lower premium/higher deductible plan.

out of pocket maximum: this is the cap on how much– aside from premiums– you should have to pay in health care costs in a year. most plans on the exchanges right now have a high deductible and higher OOP max.

network: this is the collection of providers (doctors, surgeons, urgent care facilities, imaging facilities, etc.– any clinical medical care or medical service provider) that are contracted with the insurance plan. this means that they have an agreement with the plan to accept payment from that plan for services. you can still see out of network providers, but your plan may have a separate out of network deductible that is higher and that you pay separately from your main deductible (for example, if your plan deductible if $5,000, you might have a separate out of network deductible of $5,500; even if you’ve already paid of $4,950 of your regular deductible, if you see an out of network doctor, you’re going to have to hit the $5,500 deductible in copays and whatnot before the insurance covers them fully).

most insurers have their own website that identifies what doctors are in network. sometimes you can access this without being on the plan already, sometimes you can’t. a decent, though inconsistent, workaround is to use zocdoc, where you can put in the plan type you’re thinking about switching to and see what doctors are in network. the drawback to zocdoc is that contract status is doctor-reported, so if the doctor’s office in question is slow to update, the records may be out of date.

another option to determine network availability for a specific doctor or care group is, if you’re okay hopping on the phone, to just give them a call and ask outright if they’re going to be in network for plan ___ in 2018.

if you’re like me and hate talking on the phone, the other option is that large provider groups, and a good number of smaller groups and individual providers, will often also have accepted insurances on their websites. in my experience almost all providers who have privileges at a hospital will have that listed on their pages on the hospital’s website.

copay: this is a flat fee you pay to a provider when you see them. it’s like the cover charge at a bar: you pay $20 to get in the door, and then you get the dubious honor of also paying for the drinks and food you buy inside on top of that.

coinsurance: this is a percentage charge for seeing a provider. instead of a $20 copay for the cost of the visit to see doctor bob, you’re charged, say, 10% of the total cost of all charges associated with you visit to see doctor bob. if you don’t get much done, this may only like $10; if you get a full metabolic panel run and a bunch of xrays, it might be $100.

and the plan types:

hmo: health management organization. the concept of this plan is that you have a pcp (primary care provider – your regular doctor) who functions as your primary point of contact for all medical care. if you want to see a non-pcp doctor, you have to first see your pcp, who will write you a referral to see said specialist. specialists include orthopedists, physical therapists, neurologists, ob-gyns, etc. – any provider who isn’t your pcp, basically.

hmos tend to be cheaper for you, the beneficiary

this is because of how they’re paid out: pcp doctors receive a capitation (aka, a set flat amount) payment from the insurer for each beneficiary (you) who has them as a pcp.

so, if i’m a primary care doc and i have 200 blue cross hmo patients and i get $100 per patient, i get $20,000 from blue cross, ostensibly for the cost of care provided, but the provider keeps all $20,000 even if they only end up incurring $15,000 in costs. the downside of this for you as a patient is that this encourages pcps to get a lot of people to sign up as their patients, and then to see them as little as possible/push them out to specialists for actual care, as this lowers their costs and increases their revenues.

you may end up feeling like you’re going in circles trying to get actual care because you’re getting pushed from one doctor to another.

note: hmo plans sometimes do not cover out of network providers at all.

ppo: preferred provider organization. this plan is a free for all: if they’re in network, you can go to whomever you want. they tend to be a bit pricier (almost always on premiums, 50/50 on deductibles) than hmo plans, but you’re basically paying for ease of access. you can make an appointment directly with any specialist you so choose. these plans are ideal for people like me, since i have to see orthopedists and hematologists and physical therapists pretty regularly, and going through a pcp for each of those would be a pain.

you’ll tend to have relatively low copays within the network and higher ones outside of it

unlike some hmo plans, most ppo plans will provide coverage for out of network providers, just at a less favorable rate

epo: exclusive provider organization. this is the bastard child of the hmo and ppo and is also an increasingly common option on most of the exchanges. like a ppo, no pcp or referrals are provided; however, the network tends to be narrower and you have less choice of in-network providers and, crucially, they don’t tend to cover any out of network providers except for emergencies

important note: the classification of “emergency” isn’t just “emergency situation”, but generally is limited to a proven medical emergency in which you go to an actual emergency room or emergency department.

insurers will frequently challenge ER/ED bills to confirm medical necessity because–

in their defense, since they’re meant to cover almost the entirety of emergency bills and also because one of the quantifiable measures of success in moving to value-based care that the ACA established is lowering avoidable ER/ED admissions

–they don’t want to encourage people to go the ER/ED for just anything

high deductible/catastrophic: these are exactly what they sound like– plans for healthy young people who are pretty much only going to wind up with medical costs if something terrible and, well, catastrophic, like a car accident, happens. they have low premiums and very high deductibles (often approaching ~$10,000). these are only available to people under the age of thirty, because clearly as soon as you turn thirty you must turn into a total drain on all healthcare resources 😐

so what does all of this boil down to for you and your enrollment?

start by figuring out what financial help you’re eligible for! the exchanges generally have an option at the front end of the process for you to identify your annual income and number of dependents on your plan. this will let you know if you’re eligible for a subsidy or other financial help, and, if so, how much; you should also have an option when searching through plans on the exchanges to input estimated financial help, which will adjust the premiums in the search engine.

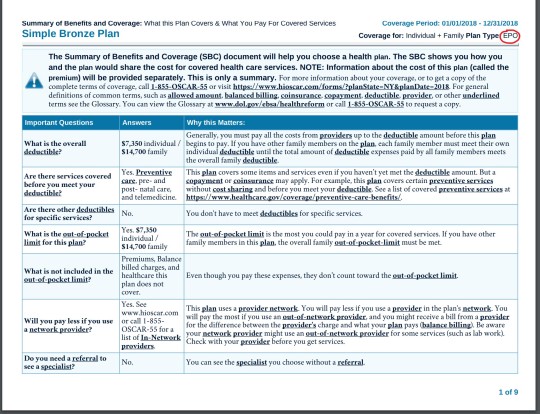

after that, start digging into the individual plan options. every exchange plan should provide a summary of benefits and coverage. it’ll be a pdf and will look like this:

that red circle in the top right there? that’s where you can identify what type of plan you’re looking at. the first page in the summary of benefits will always look the same– it’s the basic overview of the costs and definitions.

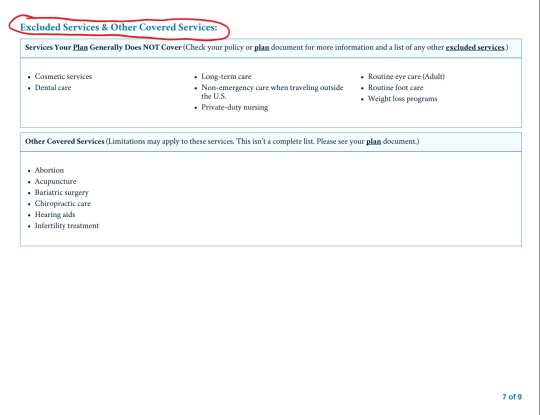

this document will also list excluded services. it’ll generally be somewhere in the middle/back half of the document and will have a clear header like this:

for me, this is the first thing i look for after verifying premium and deductible amounts. as the above picture indicates, you can find more information in the plan documents. these aren’t always directly linked to on the exchange website, but you can generally find them on the insurance providers website. these will be a lot more detailed and can be anywhere between twenty and 200 pages. ctrl + f your heart out: as frustrating and complicated as insurers can be, they can’t actually fail to disclose if they, for example, don’t cover all forms of contraceptives. they’ll disclose it in the plan documents, even if they don’t, unfortunately, have to be clear and up front about it.

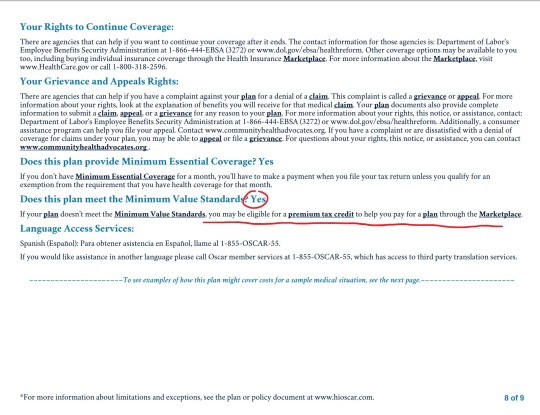

NOTE: MINIMUM VALUE STANDARDS

towards the end of the summary of benefits document will be a page that looks like this:

minimum value standards roughs out to basically meaning that at least 60% of all medical charges are covered. if the plan you’re on does not meet minimum value standards, you might be able to get a tax credit to help you buy another marketplace plan. always check for this verification when you’re researching plans.

what does all of this shit mean?

it means start here and then find your state’s exchange from there. the garbage carrot in chief established “maintenance times” on this website throughout the open enrollment period (sunday afternoons, i believe), so schedule around that. sit down on a monday or wednesday or saturday with some snacks and a cup of your favorite beer/wine/tea/whathaveyou and crank up some good music to jam to and do some research:

start with figuring out what you can afford monthly and if something terrible happens and you have to cover ER and/or surgery bills

if you have a specific doctor you want to stay with, figure out which insurances they’ll be accepting

check for coverage info in the summary of benefits documents and, if you want more detail, in the plan documents

narrow it down to a few and compare the prices

take a break and have a cookie, you deserve it at this point

pick a plan! if you’re not feeling super certain about it, go for a walk, do some laundry, pet your cat– just take a break, walk away, come back to it with fresh eyes. this is a big deal, so you don’t want to wear your brain out and give yourself a headache and then just pick one at random because you have eye strain and want to be done. open enrollment goes until december 15, so don’t rush yourself.

sign up for your plan

have another cookie and pat yourself on the back, because you just signed up for health insurance for 2018!

now take a nap because that was fucking exhausting and you deserve it

if i don’t know the answer, i can point you towards someone or some resource that will. don’t be afraid to ask me or anyone else for help! this is a complicated situation and even though the current administration is trying really hard to make it worse, there are still always resources available to you for help and guidance. all you have to do is ask 🙂

If anyone needs any help please ask me! I am a tax professional and can translate what might be confusing.

A new book has just been released by Cambridge University Press entitled Women’s Writing of Ancient Mesopotamia An Anthology of the Earliest Female Authors!

It is an anthology of translations from the ancient Near East of various writings by women. The translations include letters, religious hymns, inscriptions, prophecies, and various other types of texts. All of them considered some of the earliest examples of writing done by women in history. The only downside is that the book is quite expensive right, but hopefully that will change in the future and/or a paperback edition will soon follow.