so it’s open enrollment time, which means you need to pick a health insurance plan from the exchanges! it can be daunting as shit, for sure, especially if you don’t live in the filthy weeds that are the business side of our garbage health care industry like yours truly does.

so! here’s a quick rundown of some of the vocabulary:

premiums: this is what you pay per month for the glorious honor of having insurance coverage. it does not count towards your deductible or out of pocket maximum. depending on your income, you may be eligible for a subsidy or other financial assistance to make your premiums more affordable.

deductible: this is how much in health care costs you have to pay before your insurance starts really kicking in. for example, my insurance through work had a $1,500 deductible, so the copays and coinsurances and lab costs that i had to pay early in the year, before i had another surgery, were fully my responsibility until i’d paid out $1,500; after that, my insurance started covering a flat 80% of everything, including copays. basically, the deductible is how many actual dollars you have to pay out for medical costs before your insurance takes over.

if you’re someone who goes to the doctor a lot, like me, you’re probably going to want a plan with a lower deductible, which will have a higher premium; however, in the long run, you’ll come out more ahead with a high premium/lower deductible.

on the flip side, if you’re generally healthy and just need an annual checkup, flu shot, ob-gyn annual, etc., then you probably want a lower premium/higher deductible plan.

out of pocket maximum: this is the cap on how much– aside from premiums– you should have to pay in health care costs in a year. most plans on the exchanges right now have a high deductible and higher OOP max.

network: this is the collection of providers (doctors, surgeons, urgent care facilities, imaging facilities, etc.– any clinical medical care or medical service provider) that are contracted with the insurance plan. this means that they have an agreement with the plan to accept payment from that plan for services. you can still see out of network providers, but your plan may have a separate out of network deductible that is higher and that you pay separately from your main deductible (for example, if your plan deductible if $5,000, you might have a separate out of network deductible of $5,500; even if you’ve already paid of $4,950 of your regular deductible, if you see an out of network doctor, you’re going to have to hit the $5,500 deductible in copays and whatnot before the insurance covers them fully).

most insurers have their own website that identifies what doctors are in network. sometimes you can access this without being on the plan already, sometimes you can’t. a decent, though inconsistent, workaround is to use zocdoc, where you can put in the plan type you’re thinking about switching to and see what doctors are in network. the drawback to zocdoc is that contract status is doctor-reported, so if the doctor’s office in question is slow to update, the records may be out of date.

another option to determine network availability for a specific doctor or care group is, if you’re okay hopping on the phone, to just give them a call and ask outright if they’re going to be in network for plan ___ in 2018.

if you’re like me and hate talking on the phone, the other option is that large provider groups, and a good number of smaller groups and individual providers, will often also have accepted insurances on their websites. in my experience almost all providers who have privileges at a hospital will have that listed on their pages on the hospital’s website.

copay: this is a flat fee you pay to a provider when you see them. it’s like the cover charge at a bar: you pay $20 to get in the door, and then you get the dubious honor of also paying for the drinks and food you buy inside on top of that.

coinsurance: this is a percentage charge for seeing a provider. instead of a $20 copay for the cost of the visit to see doctor bob, you’re charged, say, 10% of the total cost of all charges associated with you visit to see doctor bob. if you don’t get much done, this may only like $10; if you get a full metabolic panel run and a bunch of xrays, it might be $100.

and the plan types:

hmo: health management organization. the concept of this plan is that you have a pcp (primary care provider – your regular doctor) who functions as your primary point of contact for all medical care. if you want to see a non-pcp doctor, you have to first see your pcp, who will write you a referral to see said specialist. specialists include orthopedists, physical therapists, neurologists, ob-gyns, etc. – any provider who isn’t your pcp, basically.

hmos tend to be cheaper for you, the beneficiary

this is because of how they’re paid out: pcp doctors receive a capitation (aka, a set flat amount) payment from the insurer for each beneficiary (you) who has them as a pcp.

so, if i’m a primary care doc and i have 200 blue cross hmo patients and i get $100 per patient, i get $20,000 from blue cross, ostensibly for the cost of care provided, but the provider keeps all $20,000 even if they only end up incurring $15,000 in costs. the downside of this for you as a patient is that this encourages pcps to get a lot of people to sign up as their patients, and then to see them as little as possible/push them out to specialists for actual care, as this lowers their costs and increases their revenues.

you may end up feeling like you’re going in circles trying to get actual care because you’re getting pushed from one doctor to another.

note: hmo plans sometimes do not cover out of network providers at all.

ppo: preferred provider organization. this plan is a free for all: if they’re in network, you can go to whomever you want. they tend to be a bit pricier (almost always on premiums, 50/50 on deductibles) than hmo plans, but you’re basically paying for ease of access. you can make an appointment directly with any specialist you so choose. these plans are ideal for people like me, since i have to see orthopedists and hematologists and physical therapists pretty regularly, and going through a pcp for each of those would be a pain.

you’ll tend to have relatively low copays within the network and higher ones outside of it

unlike some hmo plans, most ppo plans will provide coverage for out of network providers, just at a less favorable rate

epo: exclusive provider organization. this is the bastard child of the hmo and ppo and is also an increasingly common option on most of the exchanges. like a ppo, no pcp or referrals are provided; however, the network tends to be narrower and you have less choice of in-network providers and, crucially, they don’t tend to cover any out of network providers except for emergencies

important note: the classification of “emergency” isn’t just “emergency situation”, but generally is limited to a proven medical emergency in which you go to an actual emergency room or emergency department.

insurers will frequently challenge ER/ED bills to confirm medical necessity because–

in their defense, since they’re meant to cover almost the entirety of emergency bills and also because one of the quantifiable measures of success in moving to value-based care that the ACA established is lowering avoidable ER/ED admissions

–they don’t want to encourage people to go the ER/ED for just anything

high deductible/catastrophic: these are exactly what they sound like– plans for healthy young people who are pretty much only going to wind up with medical costs if something terrible and, well, catastrophic, like a car accident, happens. they have low premiums and very high deductibles (often approaching ~$10,000). these are only available to people under the age of thirty, because clearly as soon as you turn thirty you must turn into a total drain on all healthcare resources 😐

so what does all of this boil down to for you and your enrollment?

start by figuring out what financial help you’re eligible for! the exchanges generally have an option at the front end of the process for you to identify your annual income and number of dependents on your plan. this will let you know if you’re eligible for a subsidy or other financial help, and, if so, how much; you should also have an option when searching through plans on the exchanges to input estimated financial help, which will adjust the premiums in the search engine.

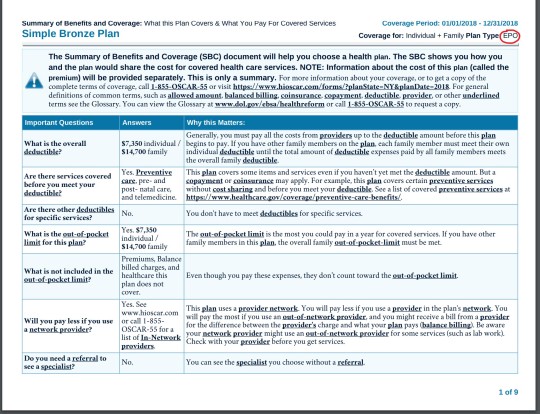

after that, start digging into the individual plan options. every exchange plan should provide a summary of benefits and coverage. it’ll be a pdf and will look like this:

that red circle in the top right there? that’s where you can identify what type of plan you’re looking at. the first page in the summary of benefits will always look the same– it’s the basic overview of the costs and definitions.

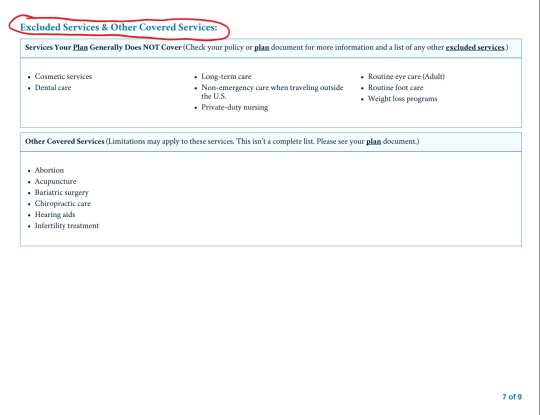

this document will also list excluded services. it’ll generally be somewhere in the middle/back half of the document and will have a clear header like this:

for me, this is the first thing i look for after verifying premium and deductible amounts. as the above picture indicates, you can find more information in the plan documents. these aren’t always directly linked to on the exchange website, but you can generally find them on the insurance providers website. these will be a lot more detailed and can be anywhere between twenty and 200 pages. ctrl + f your heart out: as frustrating and complicated as insurers can be, they can’t actually fail to disclose if they, for example, don’t cover all forms of contraceptives. they’ll disclose it in the plan documents, even if they don’t, unfortunately, have to be clear and up front about it.

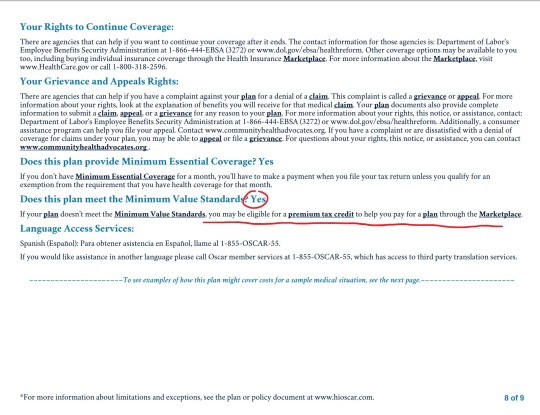

NOTE: MINIMUM VALUE STANDARDS

towards the end of the summary of benefits document will be a page that looks like this:

minimum value standards roughs out to basically meaning that at least 60% of all medical charges are covered. if the plan you’re on does not meet minimum value standards, you might be able to get a tax credit to help you buy another marketplace plan. always check for this verification when you’re researching plans.

what does all of this shit mean?

it means start here and then find your state’s exchange from there. the garbage carrot in chief established “maintenance times” on this website throughout the open enrollment period (sunday afternoons, i believe), so schedule around that. sit down on a monday or wednesday or saturday with some snacks and a cup of your favorite beer/wine/tea/whathaveyou and crank up some good music to jam to and do some research:

start with figuring out what you can afford monthly and if something terrible happens and you have to cover ER and/or surgery bills

if you have a specific doctor you want to stay with, figure out which insurances they’ll be accepting

check for coverage info in the summary of benefits documents and, if you want more detail, in the plan documents

narrow it down to a few and compare the prices

take a break and have a cookie, you deserve it at this point

pick a plan! if you’re not feeling super certain about it, go for a walk, do some laundry, pet your cat– just take a break, walk away, come back to it with fresh eyes. this is a big deal, so you don’t want to wear your brain out and give yourself a headache and then just pick one at random because you have eye strain and want to be done. open enrollment goes until december 15, so don’t rush yourself.

sign up for your plan

have another cookie and pat yourself on the back, because you just signed up for health insurance for 2018!

now take a nap because that was fucking exhausting and you deserve it

if i don’t know the answer, i can point you towards someone or some resource that will. don’t be afraid to ask me or anyone else for help! this is a complicated situation and even though the current administration is trying really hard to make it worse, there are still always resources available to you for help and guidance. all you have to do is ask 🙂

If anyone needs any help please ask me! I am a tax professional and can translate what might be confusing.

Why don’t you Google average wait times to receive a medical procedure. There are Canadians that come to the U.S. to get medical care rather than wait over a month to get it done in Canada.

I had cancer and im canadian dumbass i know full well what the wait times are like and its only long if its shit that can wait. Im sorry but im ok with waiting with a non life threatening injury if no one gets turned away from healthcare because they’re poor. The only canadians that go to the united states are rich enough that they are willing to spend the money to save a few hours waiting

Except people with life threatening injuries have to wait as well. My father had to go to the ER because the screws in his knee busted making his stitches rip open and my parents waited for hours before finally leaving when they noticed an elderly woman with a head injury and broken leg waiting at least four hours BEFORE my parents arrived.

Brian Sinclair’s death was completely preventable, yet he waited 34 HOURS in the ER for treatment that would have taken 30 minutes to an hour at most.

There are pros and cons to Canada’s healthcare, and if people want to spend extra money for arguably better treatment and shorter wait lines, I’m personally going to support them any way I can.

Yeah, that happens in the US too though. Literally every single day. Go into any ER in the country at like 9:30 pm and you will see dozens of people with painful injuries waiting hours to see a doctor. People die in the US waiting to see a doctor. The only difference is that it costs them hundreds of thousands of dollars to do so.

I had to wait six months to see an endocrinologist in the US and when I wanted to switch doctors I had to wait another six months to see somebody else, who are these people in the US who don’t have wait times?

(Brian Sinclair’s death, by the way? It’s a terrible tragedy… but the problem there was not that health care resources are spread too thin. It was racism. They saw a native man and assumed he was homeless and drunk, not in distress. As the study I cited above shows, racism is also a factor in US health care.)

So basically, you’re paying a lot more, at both the end-user and governmental levels… but you’re not actually getting a lot more.

Finally: You know what else Canada has that the US doesn’t? Wait time guarantees that require offering a faster alternative if they’re blown.

All those stories of Canadians coming to the US? Yeah, they’re basically made up. Even the highly shady right-wing think tank that Fuckface von Clownstick got the story from, trying to make the best possible case for privatization, only found that 1% of Canadian patients received health care abroad. One. percent. And that’s not “went to the US for health care,” that’s “received health care literally anywhere else for any reason, including just happening to be in another country when we got sick or injured.”

The actual numbers? Well, this study is old, but… out of a pool of 18 000 respondents, they found twenty who went to the US specifically for care.

Twenty. 0.11%.

They found that this data was consistent with Canadian payment records and US border region hospital data, so… yeah. It basically doesn’t happen. And when it does? Frequently that’s because there is an issue with the normal procedures in Canada… so the provincial government covers the cost of getting the patient to the US and treating them there.

I’ll take that over “you must be this rich to live” any day of the week.

It was also found Canadians who are treated in the States are far morely to be there because they became sick or injured while on vacation or are snow birds rather than they purposefully crossed the border.

‘Cause let me tell ya, as someone with a few chronic issues, if my choice is a 20 minute trip to the local hospital in bad traffic, where I’ll at least get coping treatment while I wait or an hour trip, plus border wait, to the States? Yeah, I’ll go local every time. The whole not having to shell out money thing is nice.

I also live near the second busiest hospital in BC. (Possibly Western Canada) Longest I have EVER waited is two hours.. and that was for a shot of toradol for pain treatment.

Another thing the liars above leave out is the huge number of working people in the US who just… don’t go to the doctor when they get injured. Because they know they can’t afford either the cost or the time away from work to get treatment and let it do its work. The US is filled with manual laborers -from roofers to bartenders to painters to stockers- with chronic pain conditions, un- or poorly healed injuries. How do they live with it? Every advil/tylenol/aspirin commericial tells you how. The importance of pain-meds to Pharma profits and easy availability of blackmarket opiates suggests an alternate answer.

The US is 300million people largely self-medicating their pain-management because they don’t want to lose their jobs, can’t afford to see a doctor for it, and don’t trust doctors because of previous bad past experiences caused by the private healthcare system. These people are, effectively, stuck in life-long wait-times, yet conservative defenders of our broken system always seem to forget to mention them when the subject of public healthcare arises.

How most people with invisible illnesses are treated by health care “professionals”

The Golden Girls didn’t fuck around

pls watch

honestly i really appreciated this scene when I first saw it bc it took me like two years to get a diagnosis for what’s wrong with me

Dorothy: Dr. Budd?

Dr. Budd: Yes?

Dorothy: You probably don’t remember me, but you told me I wasn’t sick. Do you remember? You told me I was just getting old.

Dr. Budd: I’m sorry, I really don’t–

Dorothy: Remember. Maybe you’re getting old. That’s a little joke. Well, I tell you, Dr. Budd, I really am sick. I have chronic fatigue syndrome. That is a real illness. You can check with the Center for Disease Control.

Dr. Budd: Huh. Well, I’m sorry about that.

Dorothy: Well, I’m glad! At least I know I have something.

Dr. Budd: I’m sure. Well, nice seeing you.

Dorothy: Not so fast. There are some things I have to say. There are a lot of things that I have to say. Words can’t express what I have to say. [tearing up] What I went through, what you put me through—I can’t do this in a restaurant.

Dr. Budd: Good!

Dorothy: But I will!

Dr. Budd’s date: Louis, who is this person?

Dr. Budd: Look, Miss–

Dorothy: Sit. I sat for you long enough. Dr. Budd, I came to you sick—sick and scared—and you dismissed me. You didn’t have the answer, and instead of saying “I’m sorry, I don’t know what’s wrong with you,” you made me feel crazy, like I had made it all up. You dismissed me! You made me feel like a child, a fool, a neurotic who was wasting your precious time. Is that your caring profession? Is that healing? No one deserves that kind of treatment, Dr. Budd, no one. I suspect had I been a man, I might have been taken a bit more seriously, and not told to go to a hairdresser.

Dr. Budd: Look, I am not going to sit here anymore–

Dr. Budd’s date: Shut up, Louis.

Dorothy: I don’t know where you doctors lose your humanity, but you lose it. You know, if all of you, at the beginning of your careers, could get very sick and very scared for a while, you’d probably learn more from that than anything else. You’d better start listening to your patients. They need to be heard. They need caring. They need compassion. They need attending to. You know, someday, Dr. Budd, you’re gonna be on the other side of the table, and as angry as I am, and as angry as I always will be, I still wish you a better doctor than you were to me.

Reblogging for any of my mutuals who’ve ever dealt with Dr. Budd.

Blogging this tweet because this explains SO MUCH about the mindset of pretty much all the folks I’ve known who’re against single-payer, it’s not even funny…

This….

This never occurred to me. Not once. That Americans are against Health Care because they think it actually costs tens of thousands of dollars for a broken arm, hundreds of thousands for a complicated birth, millions for cancer treatment.

Because they’ve never known anything different. The idea that a broken arm is only a couple hundred bucks; a complicated birth a couple thousand; cancer treatment only tens of thousands; all easily covered by existing tax structures.

This explains a lot. And it’s a good example of what I was talking about in my post on scarcity being used to prop up ableism – always question the idea that a resource is genuinely scarce. Even if it seems obvious that it is, quite often that’s the result of careful manipulation and misconceptions that you’re not even aware of.

And never think you’re too smart to be fooled by that kind of thing, it doesn’t work like that. Similarly, don’t think people who are fooled by something are stupid. Nobody can have all the information about everything, and nobody has the time and energy to investigate and put together conscious conclusions about every piece of information they’re given. It doesn’t take being stupid, or even just gullible, to believe something like this.

I currently live in a country without free medical care and still, it’s enormously cheap compared to the USA. An American expat wrote a piece for our English language paper about how she paid more for parking at the hospital than giving birth to her baby that’s pretty interesting:

Yesterday I had to go to the hospital cause I injured my eye, I’m frankly dreading what the bill is going to be, but what made me balk was being told in the pharmacy that my insurance was denied for the antibiotic eye drops and it’d be over $100 out of pocket. So I didn’t get my eyedrops.

I’ve had these same drops before living in the UK. They cost me seven GBP.

It’s the exact same drug, same steroid, same strain of antibiotic. But somehow the US gets away with charging $100 for a generic non brand version of a drug which is easy to create and widely used. It’s downright robbery, but also a form of eugenics through poverty and class warfare. You keep the poor poor by making sure basic necessities remain unattainable and then you make it seem like the norm so no one fights it.

Blogging this tweet because this explains SO MUCH about the mindset of pretty much all the folks I’ve known who’re against single-payer, it’s not even funny…

This is an important thing to point out to people who aren’t aware of it!